Students

My courses,master program and PhD thesis:

In the first year of the master program students will deliver weekly seminars where the basics of stochastic calculus or Markov chains will be exposed from a mathematical point of view. Here are some of the topics where I may direct master and doctor dissertations. If you want more information, please contact me. Malliavin Calculus in Finance. Monte Carlo simulation. Error analysis. Insider trading. Lower bound estimates for densities of random variables in Wiener space. Simulation methods in Finance. SDE's with irregular coefficients

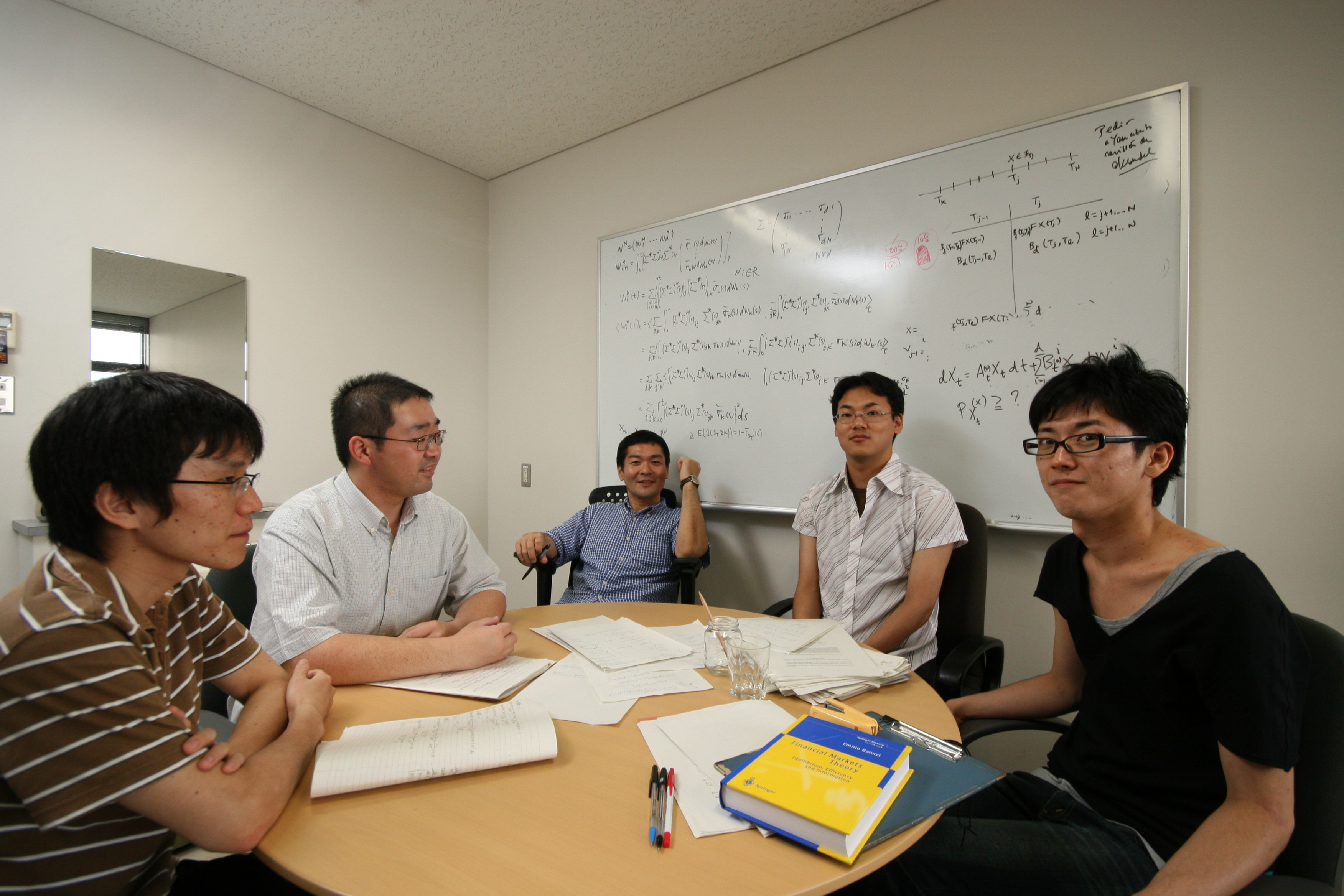

Here I am with some of my students(Photo Courtery of Nikkei BP Planning).Years later they are `respectable members of society'.

A personal statement about doing the master/PhD program in Mathematical Finance at Ritsumeikan University

Research statement for prospective Master/PhD students.

My research concern various areas that relate to mathematical finance and probability theory.

They can be shortly resumed as in the web page statement:

- Malliavin Calculus in Finance.

- Monte Carlo simulation.

- Error analysis.

- Insider trading.

- SDE's with irregular coefficients.

- Although some of the above titles may lead you to believe that there is no need of deep mathematics to do research in these topics.

The research group that I belong to (together with Prof. Akahori, Prof. Yasutomi, Prof.Owari, Prof. Nakatsu, Prof. Koyama, see complete list on the webpages of the department or Prof. Akahori's ) is dedicated to the study of real problems using mathematical probability theory.

We welcome students that are interested in studying applied problems with a powerful mathematical theory. We usually start working with students on the 4th year seminar. The topics in the seminar include Markov chains, basic (measure theory based) probability theory, mathematical finance between others. It is important that students at this level realize the difference between doing theoretical mathematics and applications. In fact, these two points of view go hand in hand complement each other but one can not rely only on one of them and forget the other. Keeping this in mind is important. Seminars are done on the mathematical theory level but the application scenery should be also understood..

In the first year of the master one may study

- Durrett Stochastic Calculus

- ÆĘłõ

- Kallenberg Foundations of Modern Probability(way too difficult)

- Prof. Watanabe's book

- Bass's book on Stochastic Processes

- Prof. Sekine's book on Mathematical Finance

One example: One of my interests is Malliavin Calculus. Malliavin Calculus is based on the integration by parts formula in infinite dimensional space. To do this one needs to have an appropiate measure on that space. That measure is provided by the Wiener process or Brownian motion.

Studying this theory is not easy but it is extremely interesting. In fact, recently due to computational needs in Finance, one can apply this theory to obtain formulas that can simulate the greeks (as they are known in Finance). Greeks are quantities that measure risk in certain financial positions. Therefore the highly theoretical framework of Malliavin Calculus can give some interesting answers to these problems. In fact, some financial institutions use this technique to compute some greeks in reality. Therefore theory and practice are not too far away. A usual master thesis written under my direction, contains a theoretical part and if possible (time allowing) an application that can be usually obtained through computer simulation. The type of work during the second year of the master is through direct interaction with me. Usually there is no seminar structure as I expect you to be able to do some independent work. Nevertheless, I am always available for discussion.

So the required skills to be a student in Mathematical Finance is to have- 1. A strong mathematical background and interest in mathematics in general.

- 2. If possible (not completely required), some computer programming skills (such as C programming).

- 3. Be willing to prepare by yourself (if you have not taken the appropiate courses) in basic probability theory, (Borel Cantelli lemma, convergence in probability, almost surely and in distribution, strong law of large numbers, central limit theorem etc. ) and discrete time martingales.