学生の生活

コハツ研究室の学生について

学部生

学部3年後期の研究室配属の後、3回生の春休み前からセミナーを始めます。立命館大学の確率論グループ全体として、1人ずつがD.Williams "Probability with Martingales"やJacod & Protter "Probability Essentials"などの個別セミナーを通して、測度論に基づく確率論・離散確率過程についての理解を深めていきます。 学部4年生では、それと並行し別のテーマのコハツ研輪講ゼミを行います。2012年度、2013年度の4回生のゼミでは、

- マルコフ連鎖

- 数理ファイナンス

をテーマにして、コハツ研全体でこれらの知識を共有します。また、秋頃からはレヴィ過程に関するノートを使って、修士1年目の夏くらいまでレヴィ過程と呼ばれる確率過程についてゼミを行っていきます。

修士

学部卒業~修士1年目の夏を目途に、個別セミナーの本を終え、2冊目に取り組むことになります。 現在のM1,M2,卒業生がこれまで2冊目として読んできた(読んでいる本は)

- 長井英夫「確率微分方程式」(共立出版)テスト

- 渡部信三「確率微分方程式」(産業図書)

- 関根順「数理ファイナンス」(培風館)

- Karatzas and Shreve "Brownian Motion and Stochastic Calculus" 2nd ed.(Springer)

- Olav Kallenberg "Foundations of Modern Probability" 2nd ed. (Springer)

- Richard Durrett "Stochastic Calculus" (CRC Press)

- Richard F. Bass "Stochastic Processes" (Cambridge)

- Avner Friedman "Stochastic Differential Equations and Applications" (Dover)

- Dieter Sondermann "Introduction to Stochastic Calculus for Finance" (Springer)

などです。 コハツ研究室では、指導教官と学生との間でのディスカッションを大事にしています。毎週や毎日といった定期的な共有ではなく、学生が研究の中で進展したこと、つまずいた疑問点・問題点を見つけるごとに、指導教官と議論をして、研究を進めていきます。そして、以下のテーマを中心に修士や博士の論文を作成していくことになります。(テーマについて詳しく知りたければご連絡ください)

- ファイナンスに関するマリアヴァン解析

- モンテカルロシミュレーション

- 誤差評価

- インサイダー取引

- ウィーナー空間上の確率変数の密度に対する下からの評価

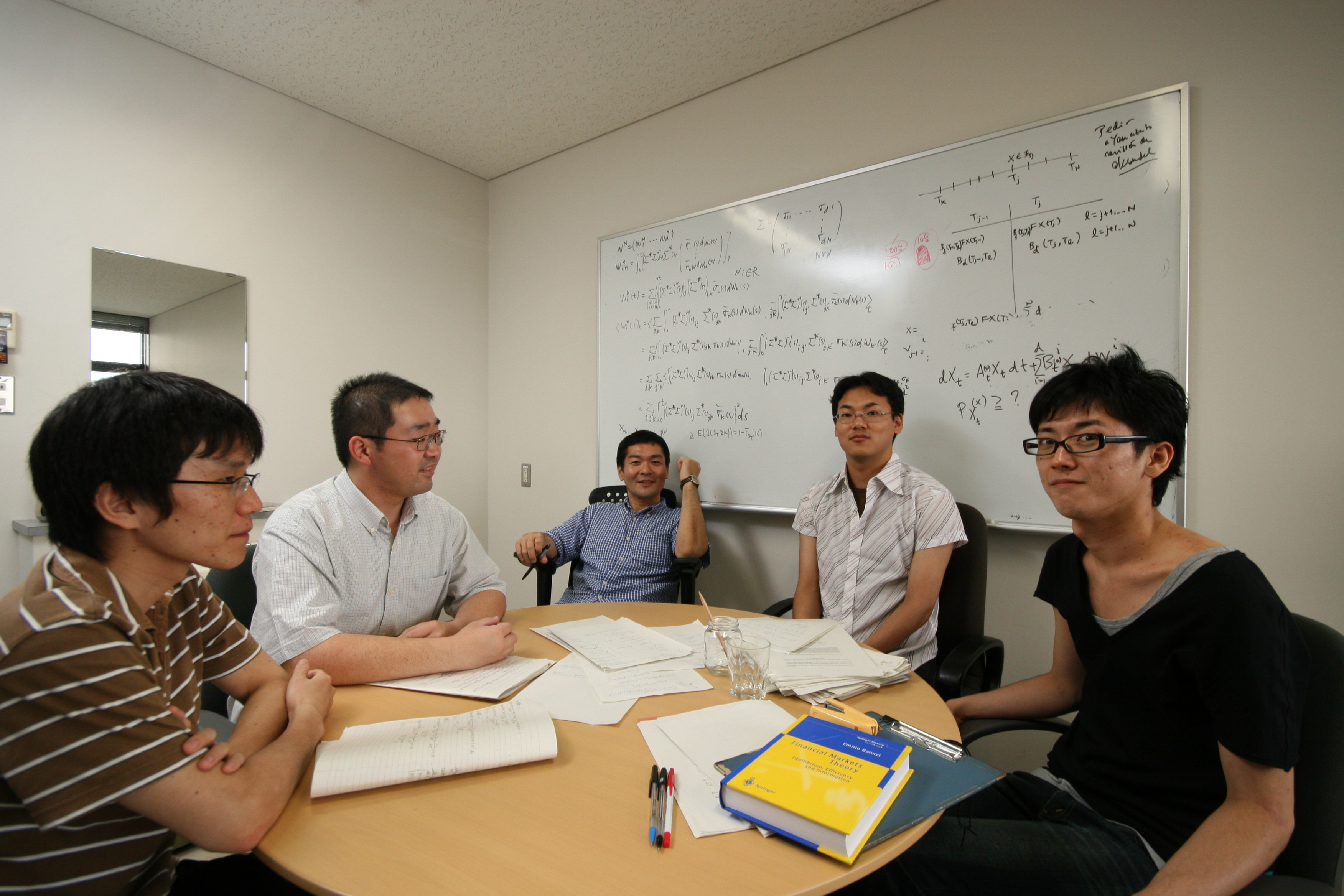

大阪大学に在籍していたときの学生との写真(左)と立命館大学のコハツ研究室内の写真(右)

Studying this theory is not easy but it is extremely interesting. In fact, recently due to computational needs in Finance, one can apply this theory to obtain formulas that can simulate the greeks (as they are known in Finance). Greeks are quantities that measure risk in certain financial positions. Therefore the highly theoretical framework of Malliavin Calculus can give some interesting answers to these problems. In fact, some financial institutions use this technique to compute some greeks in reality. Therefore theory and practice are not too far away. A usual master thesis written under my direction, contains a theoretical part and if possible (time allowing) an application that can be usually obtained through computer simulation. The type of work during the second year of the master is through direct interaction with me. Usually there is no seminar structure as I expect you to be able to do some independent work. Nevertheless, I am always available for discussion.

So the required skills to be a student in Mathematical Finance is to have- 1. A strong mathematical background and interest in mathematics in general.

- 2. If possible (not completely required), some computer programming skills (such as C programming).

- 3. Be willing to prepare by yourself (if you have not taken the appropiate courses) in basic probability theory, (Borel Cantelli lemma, convergence in probability, almost surely and in distribution, strong law of large numbers, central limit theorem etc. ) and discrete time martingales.